I’m a fan of thought experiments (as anyone who reads this page regularly already knows). A thought experiment is a process by which one weighs the information that one has and considers the consequences. Doing this allows the experimenter the ability to make better choices and consider the underlying truths of a situation. Today we’ll apply this to the common practice of subdividing land and discover why it may be helpful (from a value perspective) to have an appraisal beforehand.

Imagine a 50-acre farm, with multiple farm buildings and a farmhouse at its center. The property has rolling hills and is generally a lovely place. However, the landowner, upon their death leaves the land to two sons. Both sons have no interest in keeping the whole farm, however, the younger one does want the house. A neighboring farmer has expressed interest in the property for the purposes of the land only. Perfect! There are buyers for the whole property, all that needs to be done is a subdivision, but where do we draw the lines?

The farmer only wants the land. He doesn’t want the two barns on the property, because he has his own buildings and doesn’t want the liability.

The younger brother only wants the house and no buildings.

The older brother wants the value of both to be as high as possible in order to maximize his inheritance.

Immediately we know that there is going to have to be a compromise. If the farmer has his way, he will own a doughnut-shaped property with the house and buildings in the center owned by the younger brother. Assuming that the house and buildings can sit on only 5 acres, this will leave 45 acres worth of buildings sitting on a 5-acre parcel. Think of it another way: If I have 50 acres of land, and buildings for storing the equipment needed to farm, store, tend, etc that land… what am I going to do with those massive buildings once I no longer need all of that equipment? If the subdivision happens in this way, the “functional utility” (or usefulness) of the barns drops dramatically. In terms of the appraisal problem here:

The farmer and the younger brother do not have the “Highest and Best Use” of the property in mind. They want the property cheep, and for their own purposes.

Only the older brother in this instance has the highest and best use in mind. In order to maximize the property’s value, it might be necessary to subdivide the property in accordance with the brother’s wish, to preserve the value of the barns and other buildings. It might also be necessary to wait and sell to another party that wants the whole property as is.

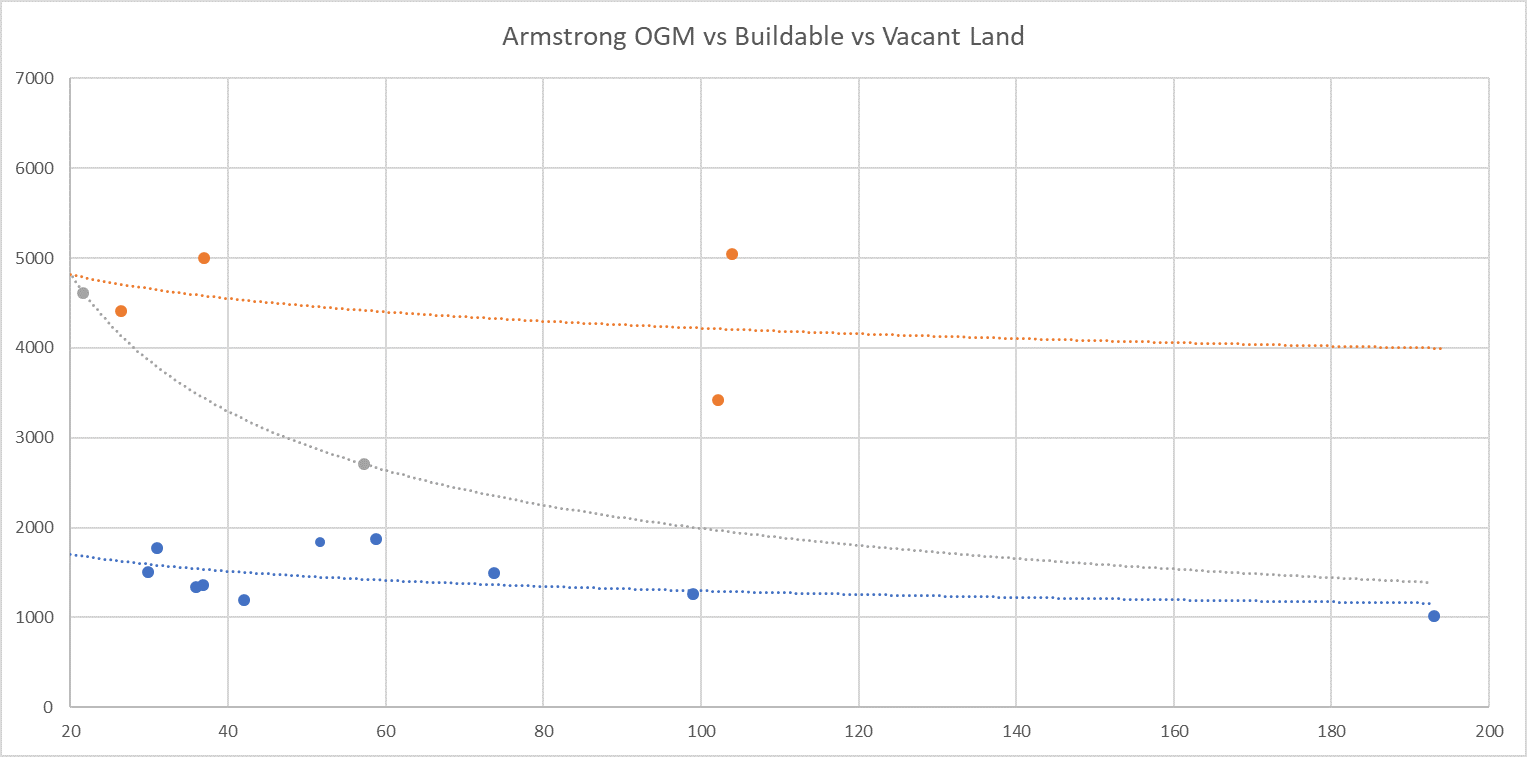

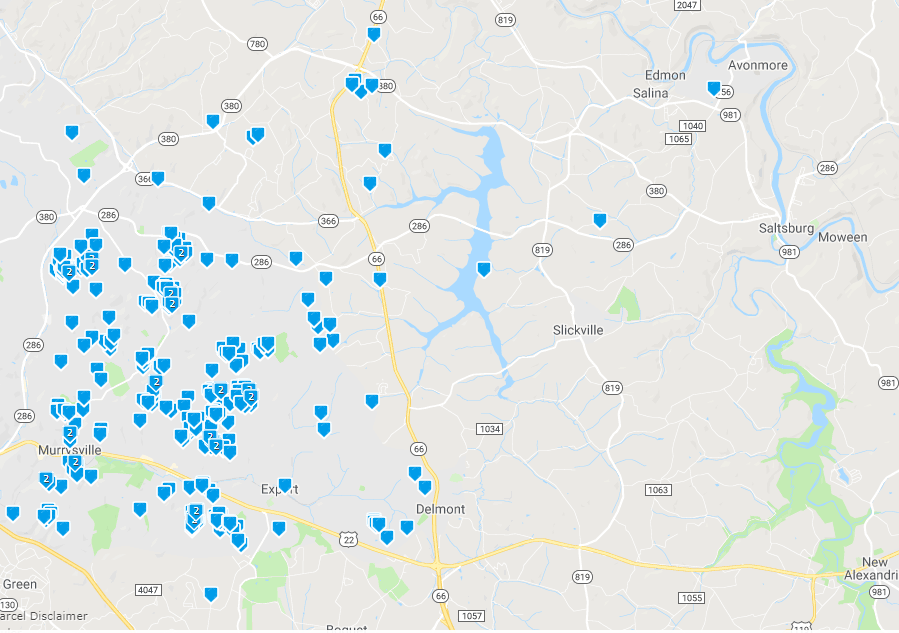

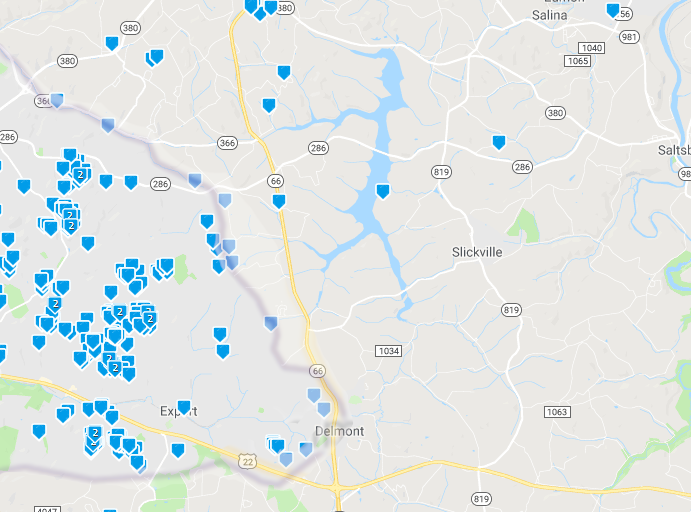

Luckily for us, in rural western PA, we have the case study of what happens when this type of situation occurs.

What you see here is a 48.66-acre farm that was subdivided, with a 5-acre parcel removed from the middle. All of the farm’s improvements are on the 5-acre parcel, and there is little room for a hobby sized vegetable garden on the remaining land, much less a farm that would need two large barns with areas for livestock plus other buildings. When this subdivision was made, the usefulness of the outbuildings on the 5 acres of land went to nearly 0. Unless the highest and best use of a commercial venue (rustic farm weddings perhaps) is envisioned, it’s hard to imagine the typical buyer seeing these buildings as anything more than a liability.

How could this be corrected?

The owner of the home could seek to sell the buildings to the farmer of the other land.

The owner of the home could purchase the farmland back, thus restoring the utility of the outbuildings of their site.

If you find yourself in need of a subdivision, a surveyor can give you the options as to where property lines could be placed. You do need to consult with a valuation expert to determine the highest and best use of the property, the potential buyer pool of the property and what characteristics (site size, improvements, etc) that they expect. Once you have all this information, you will be best prepared to create a subdivision that not only serves the needs of each parcel being created, but gives you the highest and best use resulting in optimum value.

To demonstrate an example where there is plenty of information, go to: https://en.wikipedia.org/wiki/Klondike_Big_Inch_Land_Promotion

This was one of the strangest “subdivisions” of all time. In 1955 Quaker oats bought 19.11 acres of Yukon territory, and printed 21 million deeds of 1 square inch of land to give away with their oatmeal. They paid $1,000 for the whole 19.11 acres - but how much were 21 million square inches worth separately? Well, in as much as the entire parcel was reclaimed by Canada for failure to pay $37.20 in back taxes, its fair to say that it was probably made worthless. To put it another way, poor planning of a subdivision destroyed 100% of the value of the land.